Our marketplace of AI-enabled platforms and enablers covers currently 166 vendors. In this article we take a sneak peek inside and gather some insights about the landscape.

Our marketplace continues to grow, and although we cannot claim to list all relevant vendors with complete data coverage, we aim to maintain a comprehensive overview of the landscape.

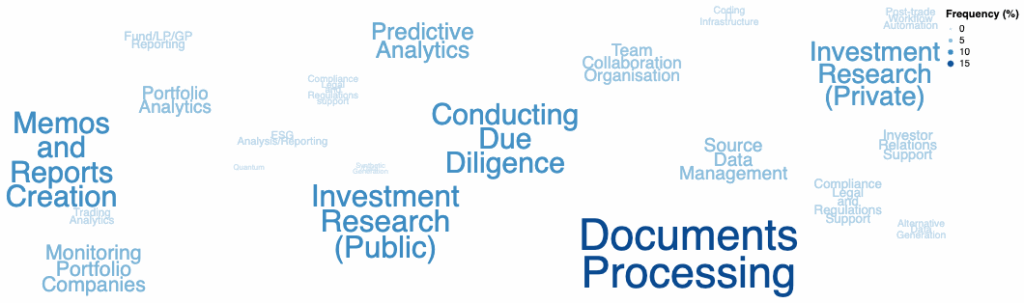

A Plethora of Use Cases

We have classified vendors across 21 use cases types (“Services”) they cover.

Use cases covered by vendors

The four main use cases covered by vendors to date in our directory are:

Memos and Reports Creation (e.g. IC memos, credit memos, research reports)

Conducting Due Diligence (e.g. due diligence on target companies)

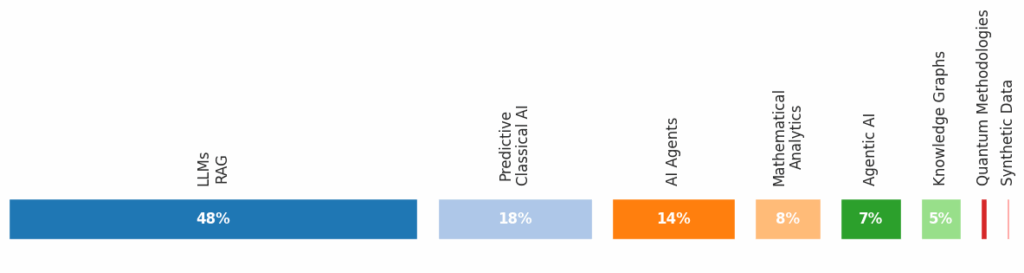

It Is Not Just About GenAI

These clearly leverage the use of LLMs as a primary technology for the vendors.As highlighted below in the breakdown of vendors’ underlying technologies: LLMs and Retrieval Augmented Generation (RAG) is used by 50% of the vendors covering these cases.

Main technologies powering vendor products

Yet Classical AI is second (mainly used for predictive analytics), followed by the more recent development of AI Agents (which are LLMs+tools+memory).

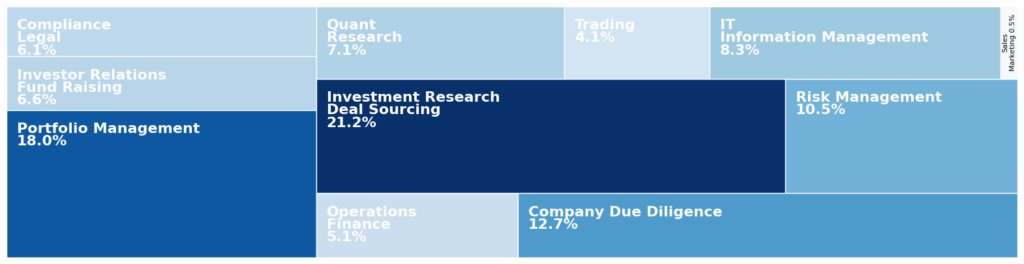

Covering All Enterprise Functions

We have identified 11 possible functions (i.e. functional areas within firms) targeted by vendors

Wide and balanced functions coverage

The four main functions covered by vendors in the directory are:

Investment Research / Deal Sourcing

Portfolio Management

Company Due Diligence

Risk Management

This is in line with the main use cases serviced by vendors described above.

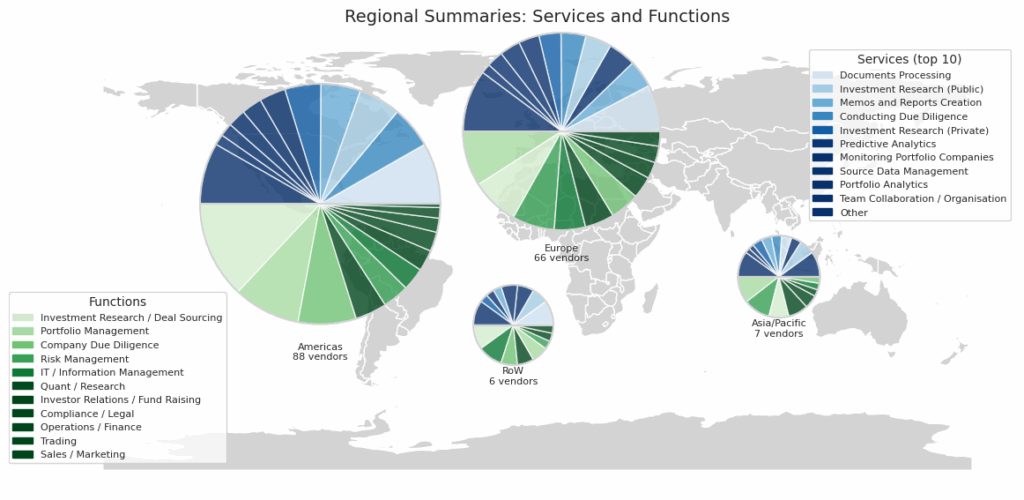

Geographical Location Matters

Despite having global reach, vendors would tend to cover markets they know best, and that usually implies the ones of closer geographic proximity. As a result there is regional variation to the services offered and functions targeted.

Different places, different problems and solutions

While Documents Processing is the main use case covered by vendors across the globe, Asia/Pacific vendors focus more on Predictive Analytics. European vendors differentiate from their American counterparts by also focusing more on Predictive analytics and automated reporting. Over the pond, vendors favour solutions that help investment decision making (DD and investment research)

Americas

Europe

Asia/Pacific

RoW

Documents Processing (17%)

Documents Processing (15%)

Predictive Analytics (20%)

Documents Processing (20%)

Conducting Due Diligence (11%)

Memos and Reports Creation (9%)

Investment Research (Public) (12%)

Investment Research (Public) (13%)

Investment Research (Public) (11%)

Predictive Analytics (9%)

Alternative Data Generation (12%)

Source Data Management (13%)

Show Me The Money

The AI landscape is shifting rapidly and is still expanding. We predict that many players will disappear as consolidation takes place in the near future or vendors are hitting the end of their runways without enough revenues. Therefore, users might prefer more established and/or well-funded vendors when deciding on transformative AI solutions for their businesses.

Based upon the information available to us including public sources and vendor-provided information, our analysis of the vendors in our marketplace shows the following on number of launches, funding and company size.

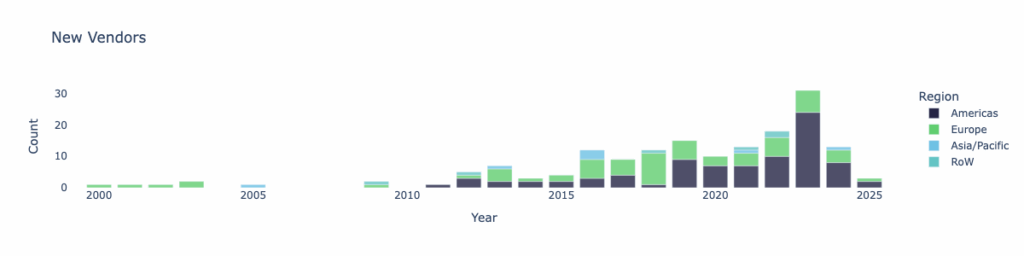

Past the peak in new vendors

Vendors are equally split between startups, defined as less than 5 years old and more established companies. The pace of new company creation has slowed significantly from the highs of 2023 when new vendors emerged every fortnight.

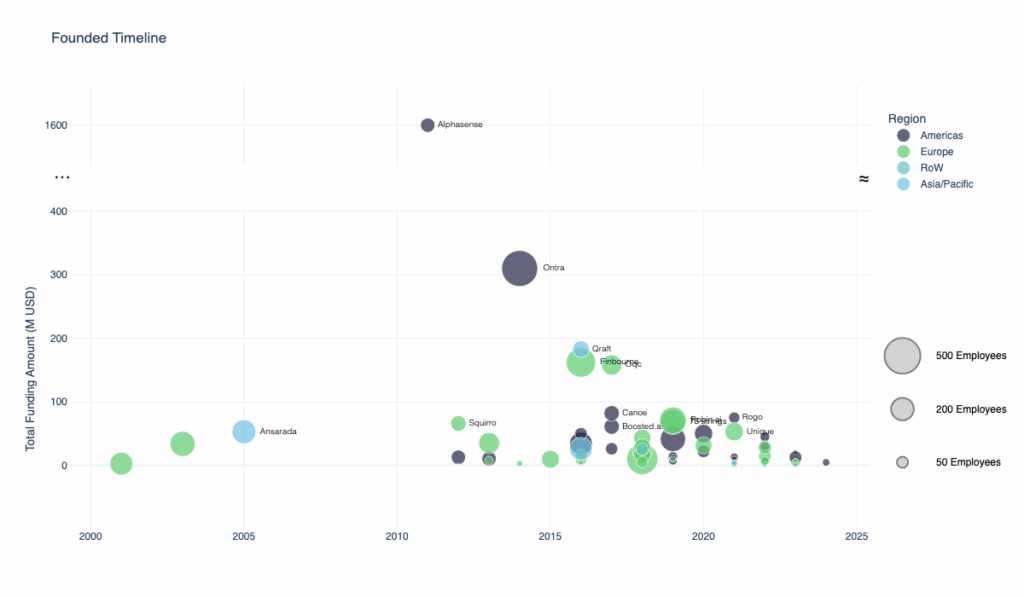

Funding according to date founded

Most companies have raised relatively modest amounts (well below under $100M), but there are notable outliers such as AlphaSense ($1.6B), which leverages its access to proprietary content to enhance investment research and Ontra ($310M) for legal/compliance. A few other companies have secured $150-200M in funding both in Europe and Asia: Qraft (AI-powered analytics), Finbourne and OQC (Quantum Computing). None of these companies are startups.

In terms of geographic distribution, the Americas dominate both in number of companies and mega-funding rounds. Europe has a strong representation with many companies, though generally smaller funding amounts while Asia/Pacific has fewer companies but some with substantial funding. The Rest of World (RoW) has limited presence.

The 2019-2023 period shows an explosion of new AI companies, likely reflecting the Deep Learning boom and increased investor interest in AI applications. However, most of these newer companies haven’t yet achieved the massive funding rounds of some earlier pioneers.

Don’t Do It Alone

While we tend to associate AI exclusively with generative AI nowadays, it also covers more classical technologies and use cases other than Natural Language Processing (with LLMs). The wide variety of the vendors in our directory reflects this.

In terms of market maturation, the data suggests the AI vendor ecosystem has evolved from a few well-funded early movers to a diverse landscape of specialised companies, with funding becoming more distributed across many players rather than concentrated in just a few giants.

The overall pattern reflects the AI industry’s transition from the experimental phase towards mainstream adoption, with increasing specialisation and geographic diversification.

Navigating this landscape is complex and requires guidance. Qaike can help you narrow down the best solutions for your business.

Disclaimer: This article is based on publicly available information and reflects Qaike’s own analysis and opinions. It is not intended to provide professional advice, endorsement, or a definitive assessment of any vendor or product. While every effort has been made to ensure accuracy, completeness and correctness cannot be guaranteed.